Are you feeling strapped for cash? Looking for a suitable crediting option? When you are in the market for a new credit card or a personal loan, you may think that only your credit score matters.

While it’s true that your score plays an important role in getting approved for credit, this isn’t the only factor lenders review.

They aim to see the full financial profile of the potential borrower when they decide which interest rate to set and whether they should approve your request.

Here are other factors they consider.

Lenders Look Beyond Your FICO Score

There are many ways to obtain emergency cash immediately today but you still need to choose the most suitable lending option and possibly avoid a hard credit inquiry.

When lenders review your application for a borrowing option, they will look at your credit score.

Your FICO score provides basic data about your creditworthiness but there is more to that apart from your rating. Some crediting companies may have their proprietary scoring models.

They may be similar to the FICO rating but still include other factors when defining a borrower’s eligibility for a certain lending tool.

It’s necessary to admit that your credit rating plays an essential role in assisting you in the application process. This is an important element that creditors will view before they make their decision.

However, additional factors such as the length of time you were employed, the sum of your regular income as well as the number of funds you have in your checking account can also help them decide if you are a responsible borrower.

More than that, you should take into consideration that being a co-signer means a person takes partial responsibility for the loan payoff.

The track record of payments on this co-signed loan becomes the track record not only of the main borrower but also of a co-signer.

Keep this information in mind next time you decide to cosign a loan for someone.

Additional Factors Lenders Consider in Your Loa Request

Credit History

The three-digit number which is calculated from the information in your credit reports is your credit rating.

This rating is used to predict your creditworthiness and how likely you will pay the debt off. However, apart from this figure lenders will also review your credit report.

This report can be obtained from one of the three major credit agencies.

Your credit history is included in this report. This is a record of how a borrower managed previous debt payments.

Crediting companies may want to search for past bankruptcy, delinquent accounts, foreclosures, unpaid collections accounts, outstanding debts, as well as the number of recent credit applications.

While you may still get approved for a loan or a credit card, having these blemishes on your credit report will define the interest rate as well.

You can access your credit report and check your credit history by visiting AnnualCreditReport.com. Check the information in this report to eliminate any errors.

Down Payment

The bank faces fewer risks if you request a smaller sum. Borrowers with a large down payment can qualify for a lower interest rate.

Poor credit holders may use this tactic if they want to boost their chances of getting approved for a loan.

Your Income

Borrowers with higher incomes also have higher chances of being approved.

Lenders view such applicants as low-risk borrowers as they can afford monthly loan payments and will most likely meet their financial obligations compared to borrowers without steady income sources.

On the other side, in case your mortgage or rent payments are too high, you may not get the cheapest rate.

The total debt-to-income ratio should be 43% or lower if you want to obtain a suitable lending offer from a certified creditor.

The Mortgage and Credit Guidelines published by the U.S. Department of Housing and Urban Development states that if one or both of the allowable ratios of 31%/43% are exceeded, the creditor must justify in the Notes section of the Loan Transfer why they believe that the mortgage shows a permissible risk.

The creditor should specify any compensation factors used to approve the loan. For EEH and EEM loans, a ratio of 33%/45% is considered acceptable.

Loan Term

Another important factor is the length of the loan. Lenders prefer a shorter repayment term as it increases the chances of on-time payments.

It’s preferable to have a shorter loan term as you will be able to return the debt faster and become financially independent.

Pay attention to the rates, though. Typically, the monthly payments will be higher.

Employment History

The present income is what lenders review when you apply for a mortgage.

Besides, some crediting companies may want to look through your employment history for the past several years. It will help them understand your income stability.

Those without steady employment face higher risks of getting rejected or offered higher rates.

Liquid Assets

Your income is utilized for debt repayment. Some creditors may want to review your liquid assets as well.

They want to check if you have any stocks, government bonds, money market accounts, or savings that may be converted into real money if necessary.

Hence, even if you have financial disruptions or get laid off, you will be able to return existing debt using your liquid assets.

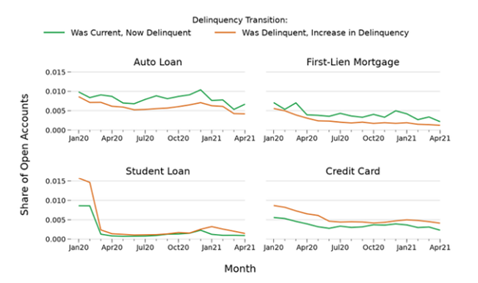

Late Payments on Credit Accounts Continue to Be Low

A recent report by Consumer Financial Protection Bureau states that delinquencies on credit accounts keep on being low despite the global pandemic. New late payments haven’t returned to 2019 levels yet.

The following chart displays the proportion of all mortgage, auto loan, credit card, and student loan accounts that went into delinquency in each month compared to the present in the previous month, and the proportion that went from a lower to a higher delinquent level.

The chart concentrates on the period from January 2020 to April 2021.

The Bottom Line

In conclusion, having a good credit rating is an important part of a successful loan application.

However, you should also consider other factors such as your employment history, your payment history, and the loan term.

Keeping your card balance low and paying the bills on time is essential if you want to boost your chances of approval.

When you demonstrate yourself as a responsible borrower with a decent credit score, more lenders will want to deal with you and offer you the best loan terms.

All of the mentioned factors can help you look good in front of potential creditors and improve your financial picture.